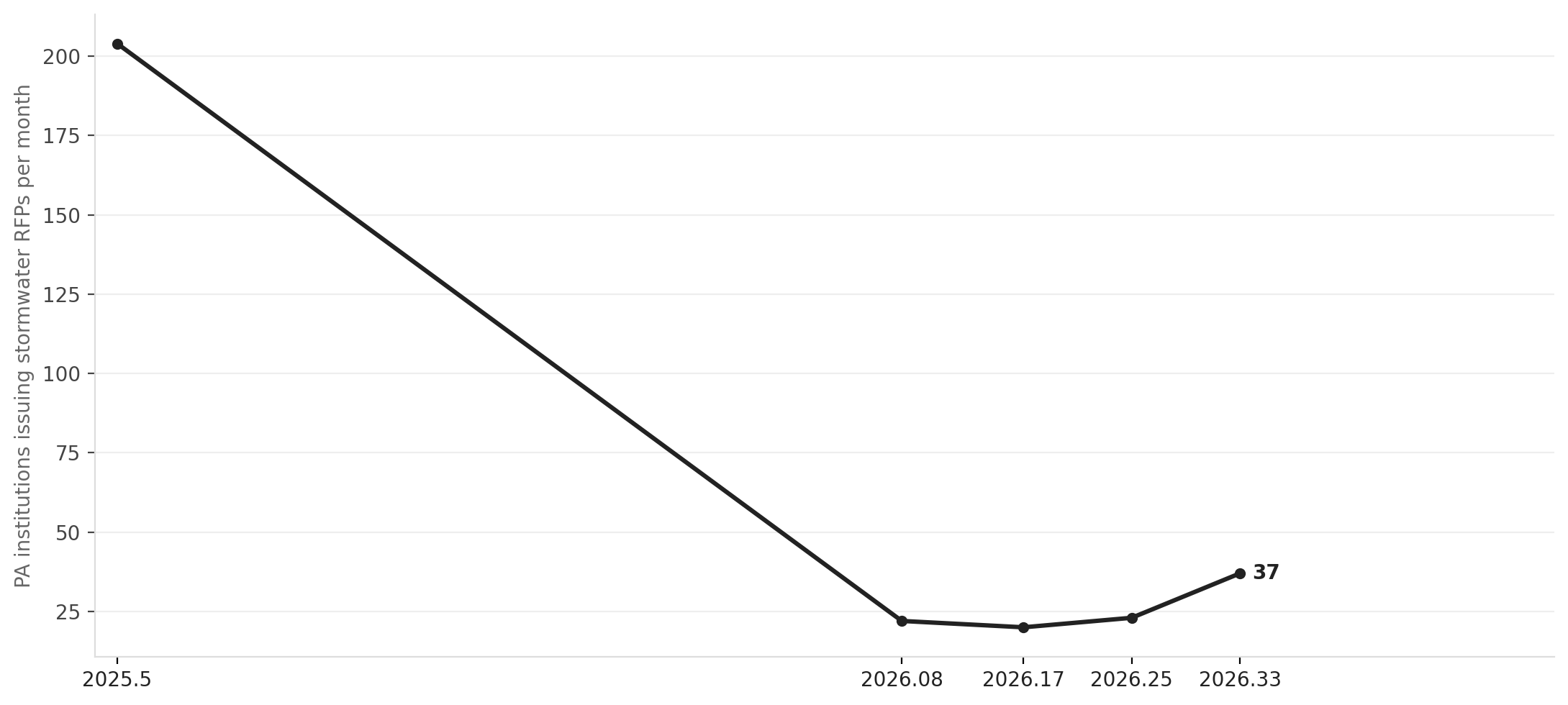

Thirty-seven Pennsylvania municipalities issued a stormwater management RFP for the first time in more than a year during the 30 days ending in late May 2026, up from zero institutions in the prior comparable window. The month produced 72 total stormwater RFPs statewide, the second-busiest single month in at least 18 months, and Pennsylvania's surge dwarfs every neighboring state: New Jersey managed 16 institutions, Maryland 11, New York 9, and Ohio 7 in the same window.

This is not a sudden enthusiasm for culverts and retention basins. It is what a regulatory deadline looks like in the public works ledger.

Pennsylvania DEP's draft reissuance of the PAG-13 NPDES General Permit, announced in the January 18, 2025 Pennsylvania Bulletin, set a September 30, 2026 deadline for all municipalities currently covered under PAG-13 to submit renewal Notices of Intent. Roughly 493 municipalities hold coverage under that permit. Miss the deadline, and a municipality loses its permit coverage entirely, a legally exposed position for any community that discharges stormwater to regulated waterways. The draft permit also introduced new requirements that didn't exist in prior cycles: a Volume Management Plan, a mandatory MEP Calculator spreadsheet that determines each community's stormwater reduction objective, and an eventual mandate to adopt a 2028 Model Stormwater Ordinance. Engineering firm RETTEW, one of Pennsylvania's leading MS4 consultants, has described the reissuance as "a significant shift in focus from pollutant reduction to volume management", meaning municipalities can't simply recycle their last permit cycle's paperwork.

Source: NationGraph.

DEP has since signaled that the final PAG-13 will not publish during 2026, which means the September 30 NOI deadline will be revised. But that news has not slowed procurement. Consultants are already mobilizing clients, scopes of work are already being written, and the RFP data shows the compliance machinery is running regardless of whether the final rule has landed.

The procurement wave has been building since February, when 22 institutions issued stormwater RFPs, rising through March (20 institutions) and April (23) before the May spike to 37. The geography is statewide. Allegheny County leads with five institutions and nine RFPs. Delaware, Chester, and Montgomery Counties each show three institutions actively procuring. Philadelphia is putting green stormwater infrastructure construction bids on the street across multiple neighborhoods. Scranton leads the state in raw RFP count, 13 RFPs tied to named neighborhood projects in Keyser Valley, East Mountain, Minooka, and along North Main Avenue.

The scale of Pennsylvania's MS4 burden explains why the numbers stand out nationally. The state has 1,059 regulated small MS4 systems, one of the largest such inventories in the country, spread across a dense patchwork of boroughs and townships many of which are under-resourced and have gone years without issuing a stormwater contract of any kind. A significant share of the 37 new entrants this month are in that category: municipalities re-entering the procurement market after a gap of 12 months or more, which is exactly the cohort most likely to be scrambling to find a consultant before the deadline window closes.

The Chesapeake Bay TMDL overlay adds another layer of urgency that most states don't face. Pennsylvania municipalities whose storm systems drain to Bay-tributary streams must submit Pollutant Reduction Plans alongside their permit renewals, connecting local pipe inspections to a federal cleanup accountability framework. That dual obligation, state permit plus federal watershed target, compresses the timeline for communities that need outside engineering help to do either.

Delaware County has taken the most organized approach so far, coordinating all 49 of its municipalities through a countywide Act 167 stormwater plan. If other counties replicate that model, the result would be coordinated procurement waves arriving county by county, which could produce RFP surges larger than anything the current monthly data shows. PENNVEST holds an active $3.18 million EPA Sewer Overflow and Stormwater Reuse Municipal Grant that municipalities can tap for compliance capital through September 2028, providing at least some financing runway for smaller communities.

The procurement surge from May represents perhaps one-tenth of the municipalities that will eventually need to move. Pennsylvania's 37 active institutions this month sit against a backdrop of nearly 500 permit holders approaching a deadline and more than 1,000 regulated systems in total. The next signal to watch is whether DEP publishes a revised NOI deadline when the final PAG-13 eventually clears, and whether that announcement produces a second spike to match or exceed last July's peak of 204 institutions in a single month.